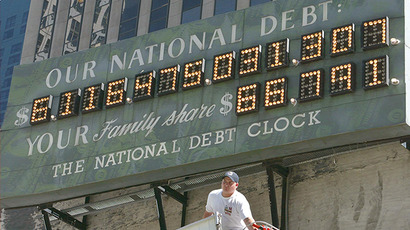

Total US debt soars to nearly $60 trn, foreshadows new recession

America - its government, businesses, and people - are nearly $60 trillion in debt, according to the latest economic data from thethe St. Louis Federal Reserve. And private debt - not government borrowing - is the biggest reason for the huge deficit.

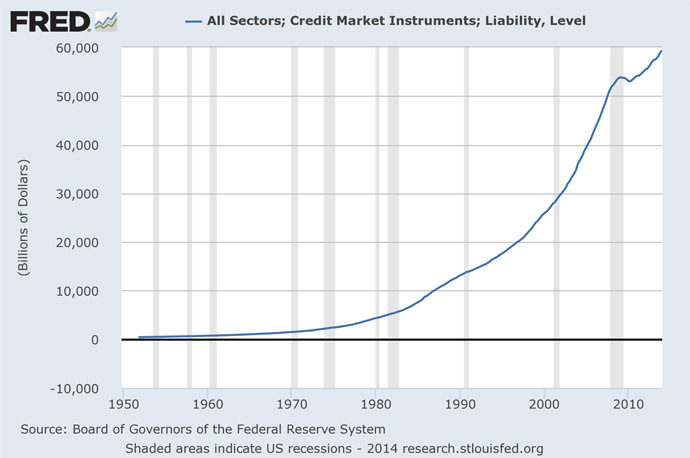

Total US debt at the end of the first quarter of 2014, on March 31 totaled almost $59.4 trillion - up nearly $500 billion from the end of the fourth quarter of 2013, according to the data. Total debt (the combination of government, business, mortgage, and consumer debt) was $2.2 trillion 40 years ago.

“In 50 short years, debt has gone from being a luxury for a few to a convenience for many to an addiction for most to a disease for all,” James Butler wrote in an Independent Voters Network (IVN) op-ed. “It is a virus that has spread to every aspect of our economy, from a consumer using a credit card to buy a $0.75 candy bar in a vending machine to a government borrowing $17 trillion to keep the lights on.”

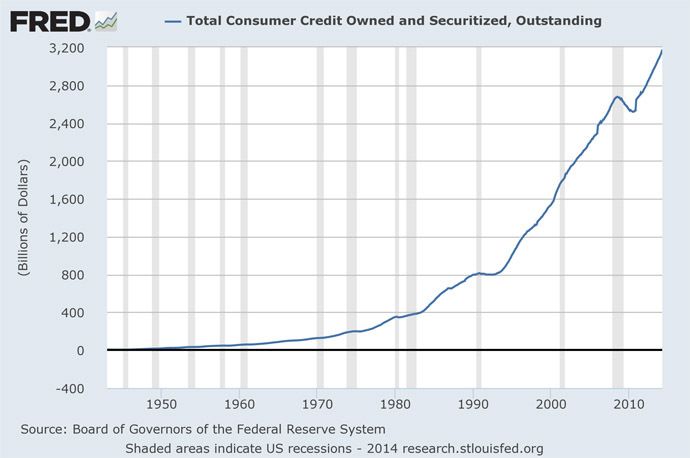

According to a 2012 study published in the Economist, rapid growth in private debt is a better predictor of recessions than increases in public debt, growth in money supply, or trade imbalances. Consumer credit in the US rose by 22 percent over the last three years, reaching a record-high $3.18 trillion in April, the Fed reported on Friday.

Credit card use (or revolving credit) rose by $8.8 billion, while non-revolving credit like auto loans and student loans made by the government surged up by $18 billion in April. Non-revolving credit jumped by 8.2 percent over the last year, while revolving credit only rose 2.2 percent over the same time period.

“For a while after the recession it was trendy to cut up your credit cards and get out of debt,” Michael Snyder wrote in an InfoWars op-ed. “But that fad wore off rather quickly, didn’t it?”

Snyder noted that 56 percent of all Americans have a subprime credit rating, and that the average monthly car payment in the US is $474. He added that 52 percent of homeowners are overextended on their mortgages and “cannot even afford the house that they are living in right now.”

Debt is hurting young adults the most. Millennials say they are spending at least half their monthly paychecks on paying off debt, a recent Wells Fargo survey found. And two years out of college, half of all graduates are still relying on their parents or other family members for some sort of financial help, according to a University of Arizona study, which also found that only 49 percent of graduates are working full-time.

"Whether or not a weak labor market is increasing the need for intergenerational support -- a likely driver in today's economy -- our data clearly showed that many young adults today may not be earning enough to make it on their own, even when working full time," the report stated.

Most of the debt that young adults face is student loan debt, which totals more than $1.2 trillion, according to the Federal Reserve. Of that debt, approximately $124 billion is more than 90 days delinquent.

“What we have done to our young people is shameful. We have encouraged them to sign up for a lifetime of debt slavery before they even understand what life is all about,” Snyder wrote.

The Congressional Budget Office predicts that the economy will stall by 2017 because Americans will continue spending, but wages and wealth won’t be going up - leading to increased income inequality in the country, the Guardian reported.

“That ever-increasing gap between income and consumption has been filled by borrowing,” the Guardian said. “These were the debt dynamics in the lead-up to the recession. But they are also the dynamics leading out of the crisis, and continuing today with no end in sight.”

Economists have not agreed on how to stave off the impending crisis. But Americans’ addiction to spending on credit will not help.

“The problem is, the more debt we have, the more future income must be used to pay the debt and its interest, which reduces the money we have to spend on things. This works to slow the economy,” Butler wrote.

“Eventually, the negative effect of the debt load becomes stronger than the positive effect of the added spending and a recession is triggered — or worse.”